Bitcoin's second near-death experience

Bitcoin has been declared dead so many times it has basically become a meme. As of the time of writing, there have been 222 obituaries proclaiming the death of the currency. I'm not here to talk about those, but about a feeling you could get from old-timer Bitcoiners.

I've been in the community since 2011, and I have experienced two moments where Bitcoin's future was uncertain. I came in right around the first notable bubble, when the price soared to the unthinkable... $30/BTC (or about ~$40 in the polish markets). After that bubble has popped, the price began to decline. Slowly creeping down, taking with it confidence of many bitcoiners. At the time nobody could tell for certain what was going to happen - whether the coins will become worthless, or will we see something different happen entirely.

People nowadays despair when Bitcoin drops 30% from all-time-high peak, but back in 2011, we saw Bitcoin go down to about $2 per coin, or a decline of about 93%. The future of the project was uncertain, everyone was depressed, and for me, that was Bitcoin's first near-death experience.

Of course, we recovered. After that, when the next bubble came, you had more confidence that Bitcoin will bounce back. We've seen it before. "There is no bubble like the 2011 bubble" I tend to say.

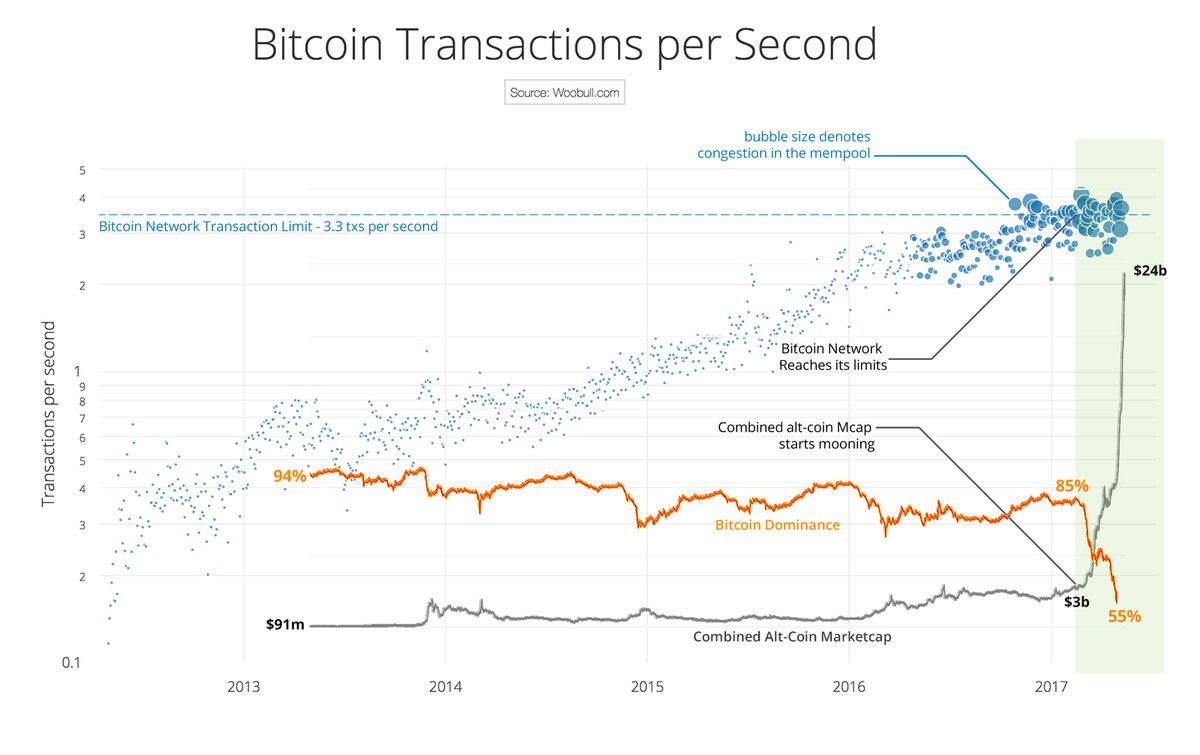

In 2017, we had to deal with the scaling problem that has been anticipated since at least 2015. We had to figure out what solution might be the best - whether to go with big blocks, or go off the chain. At the same time, we had to anticipate that ever since The DAO and Ethereum's split, any major, contentious change to the Bitcoin protocol would create a similar split. Piled on top of that we had the covert ASICBOOST scandal and over a year of the community being forcibly divided in discussing the scaling solutions.

In other words, the pressure was rising from all sides and something had to give. At the same time, many sides have remained rigid, not willing to make a compromise. Instead we saw warring solutions - SegWit, 2x, UASF, etc. In the end we saw a group trying to reach a solution - "SegWit now, 2x in half a year", which allowed SegWit to activate but would backfire when that second part was to come due.

However, before SegWit could be activated, we had a different fork be proposed - Bitcoin Cash. Increasing the block size and changing a few other things. However, this one didn't wait to reach a majority, instead opting to declare a fork happening and going through with it.

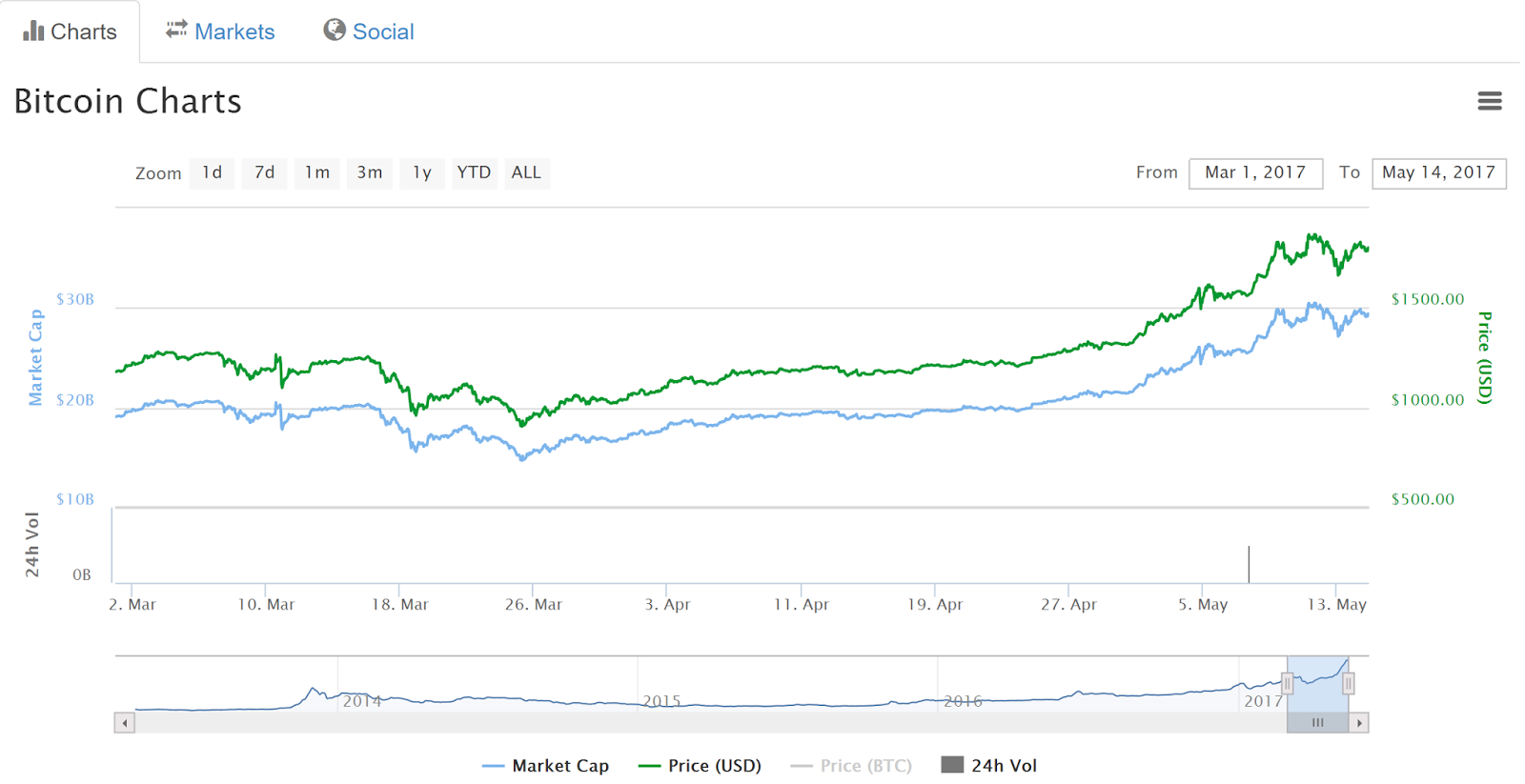

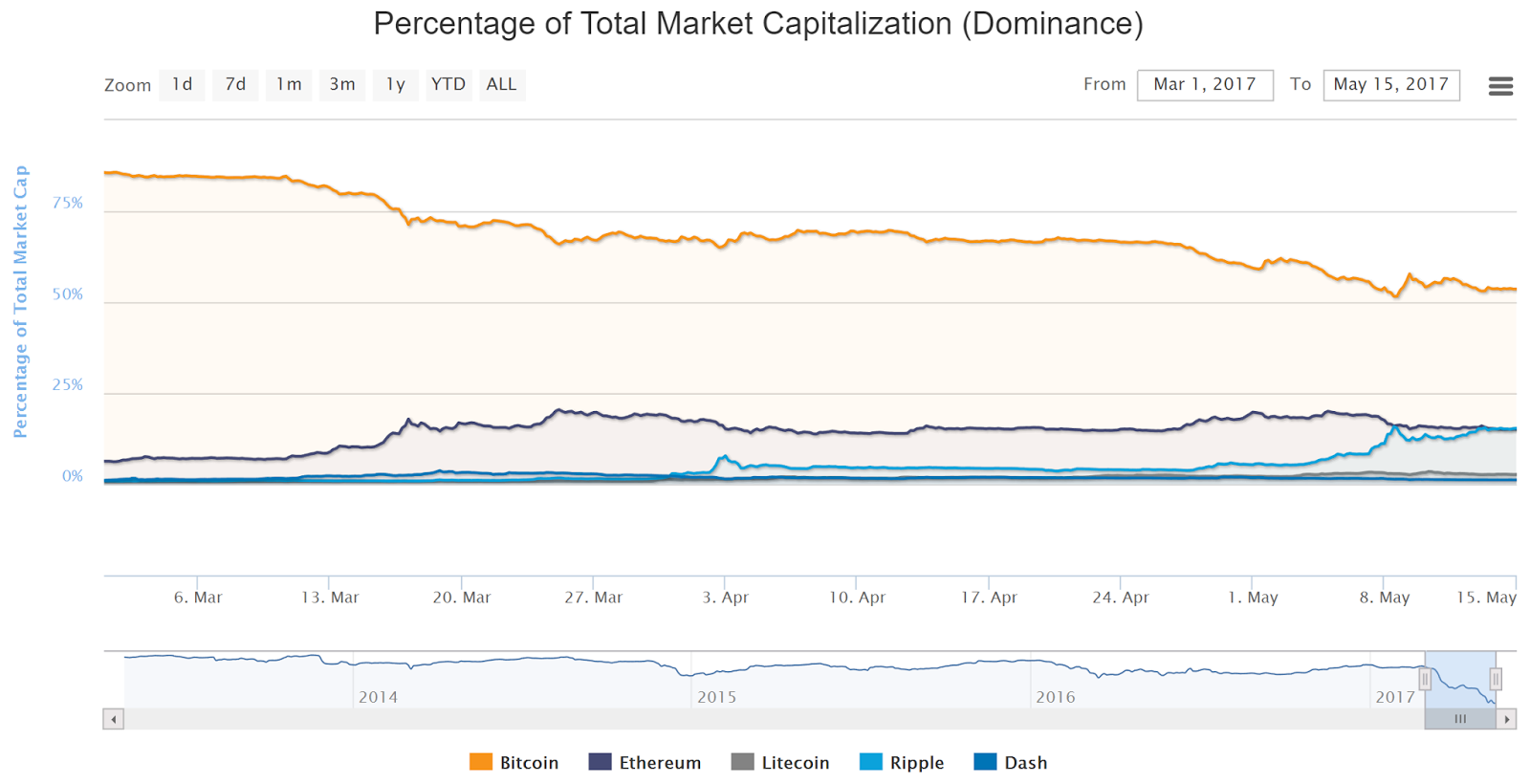

The period following the announcement has been Bitcoin's second near-death experience. The future was once again uncertain - would this split in mining power mean some crazy oscillations in the difficulty? Would the currency retain its value after the split? Would one chain dominate the other and just take over? These were uncertain times in which the altcoins thrived.

The forks came and went, Bitcoin is still around, so is Bitcoin Cash. We now know how Bitcoin responds in this situation, so we will be ready in the future once more. "There is no split like the 2017 split" I suppose?

The aftermath of the scaling debate

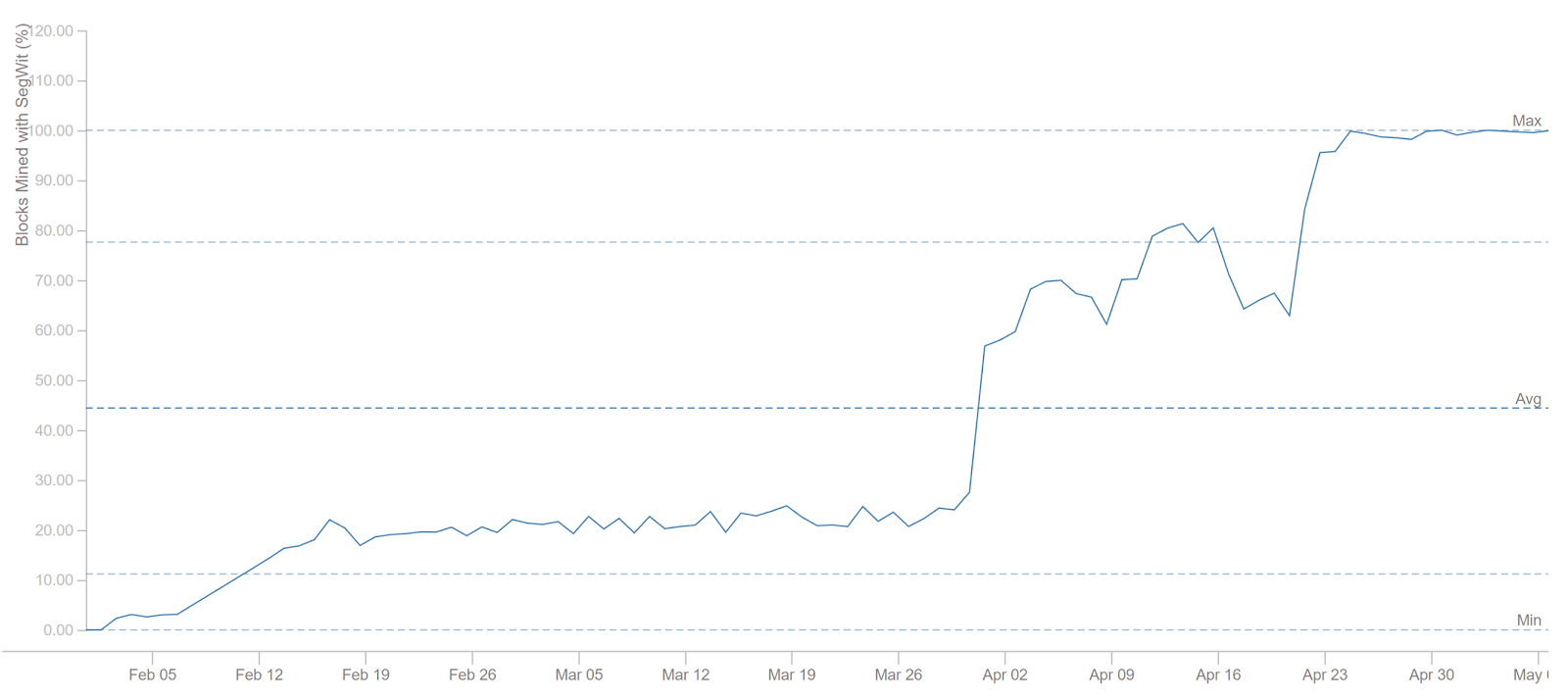

Even though SegWit has been activated, we are still seeing a lot of transactions waiting to be confirmed in the mempool. With the lightning network being months away from being ready, it seems the transaction fees will keep on increasing. We can also see an interesting trend lately - people trying to bully companies into integrating the "optional" SegWit into their system to lower fees. It's somewhat disheartening to see. I hope that in 2018 we will see an empty mempool again...

Another important event that took place this year was the failed attempt to follow through with the SegWit2x agreement and the subsequent backlash against the "transgressors". We've seen old-school bitcoiners wanting to change Bitcoin's POW to spite the miners or force various businesses to "sign a very simple pledge that acknowledges that Bitcoin is not ruled by miners in order to be linked from bitcoin.org". Luckily neither of those have gotten any traction and could be written off as a pendulum effect to the SegWit2x continuing up to the 11th hour before being called off.

The last unfortunate aftermath of the scaling debate has been the decisive split of the Bitcoin community. Up until the SegWit / Bitcoin Cash split I had hopes there could be some reconciliation (1, 2). After the scaling debate would be over and the project could be back on track that we could come back together and bury the hatchet. However, once a split happens and both sides survive long enough, there is no going back - there are people financially tied to one end but not the other that understandably won't leave their side. We had some high-profile people supporting one side or the other, and what seems like layers of narrative being spun on both sides (proclaiming something is being implemented because of X, but in reality it's done because of more selfish reason Y, for example - invading Iraq because of WMDs, while in reality it might be because of oil or the like). It's unfortunate that we have failed to keep the community together in the first place and to bring it back together before the differences were irreconcilable...

Here's to hoping we can learn to at least respect and tolerate one another and remember what we were fighting for in the first place...

Crypto securities and the SEC report

The DAO has been an important project that has already shaped the industry despite or perhaps precisely because its failing. It has split the Ethereum blockchain in twine, and this year it has given us something rather unexpected - a SEC investigative report. It concluded that The DAO has been a security, which has had a significant impact on the ICO community. Now you have to seriously consider whether you're creating a security or a utility token when creating an ICO and follow with the appropriate requirements.

This has created a new wave of interest in the community. Some people are embracing being a security and taking a full advantage of that, while others are moving away from being a pseudo-security not to be found guilty of fraud or other regulations.

The crypto-securities have definitely been dominating my conversations over the last months and I have no doubt they will be the big news in 2018. I also heard some rumours from credible sources that at least one notable project has been declared to not be a security, but I can't disclose what it is until some official announcement unfortunately. So there is development happening on both sides of the spectrum, which is always good to hear.

Conclusions

The Bitcoin scaling forks and splits have been a major event in the Bitcoin's history. They have left a lasting effect on the community and technology. This year we have also seen some important report coming from the SEC that has already began to shape the ICO landscape. We are likely to see that become a major influence of what 2018 will look like.

Here's to 2018 and what's yet to come!